Silverco Mining Releases Robust PEA for the Cusi Mine Highlighting High-Margin, Low Capital Restart

PEA Confirms Cusi Economics But Stock Lags Private Placement Price

Silverco Mining released a Preliminary Economic Assessment (PEA) for the restart of its 100% owned Cusi Mine on April 13, 2026. The study highlights an after-tax NPV (5%) of US$104.1 million in the base case (silver $44.58/oz) and US$312.2 million in the upside case (silver $75/oz). Key metrics include a 94.8% IRR, a payback period under one year (0.9 years), and an initial capital requirement of only US$19.2 million. The company forecasts average annual production of ~2.5 Moz AgEq from 2028-2033 with a life-of-mine AISC of US$26.75/AgEq oz. Management states sufficient cash on hand exists to fund the restart, and a 30,000-meter drill program is underway for resource growth.

The PEA confirms the operational thesis established during the February 2026 financing but does not fundamentally alter the investment landscape beyond validating previous guidance. - Expectations vs. Reality: The market anticipated a restart feasibility study following the US$62.5 million bought deal closed in February 2026, which was explicitly earmarked for Cusi exploration and restart work. The PEA validates that the capital raised is sufficient for the initial phase (US$19.2M capex vs. US$62.5M proceeds). - Economic Strength: The metrics are exceptionally strong for a development-stage miner (IRR >90%, Payback <1 year). However, these figures rely on a base case silver price of $44.58/oz. As a critical analyst, I note that if spot silver prices deviate significantly below this assumption, the NPV and margins compress rapidly given the high fixed costs inherent in mining operations despite the low AISC projection. - Stock Price Context: The stock is currently trading at $10.51, which is approximately 16% below the February private placement price of $12.50 where Eric Sprott and insiders invested US$10 million+. This discount suggests market skepticism regarding execution risk or broader sector weakness, despite the positive PEA numbers. - Conclusion: The news is positive as it removes technical feasibility risk, but it is categorized as Routine because the strategic path (financing -> restart) was already priced into the February rally. It confirms the plan rather than creating a new one.

- Company: Silverco Mining Ltd. (formerly Quetzal Copper Corp.) is a silver-focused mining company listed on TSX Venture (SICO) and OTCQB (SICOF).

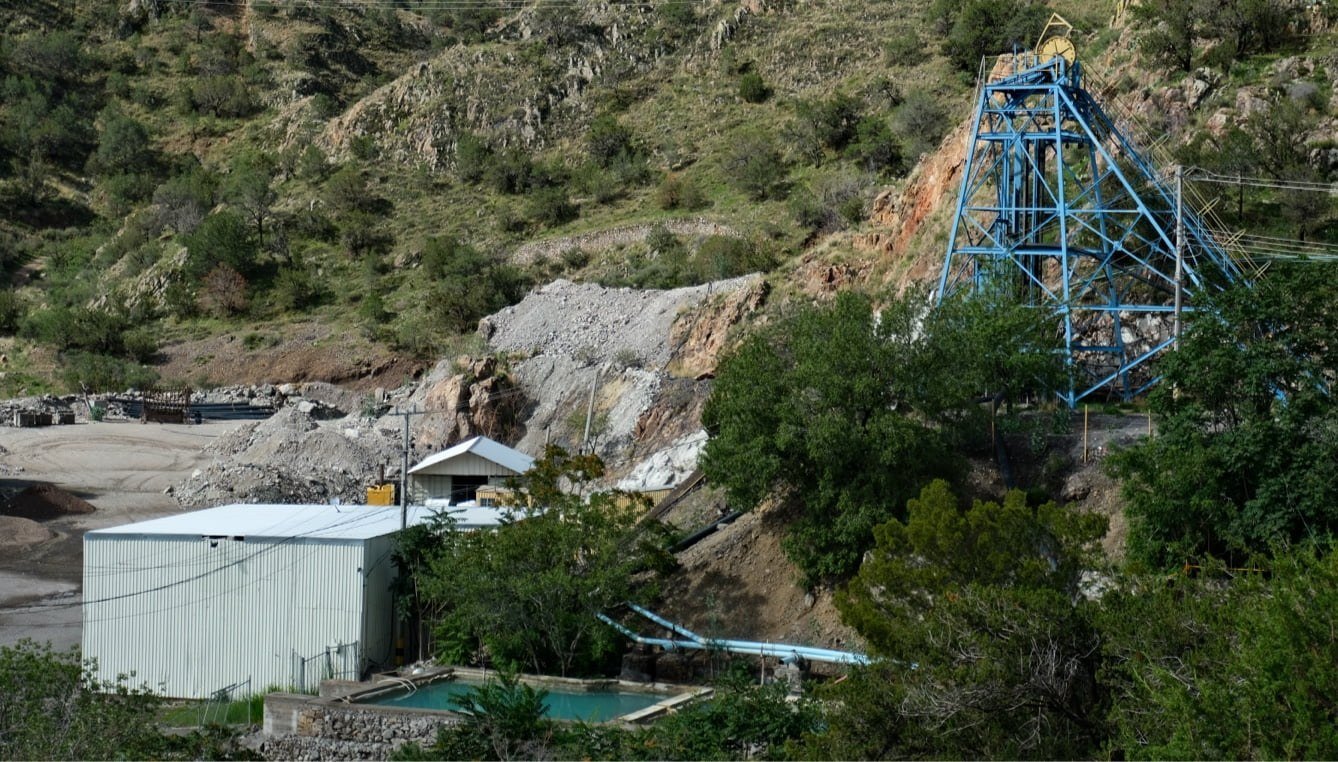

- Flagship Project: Cusi Mine, Chihuahua, Mexico. A past-producing underground silver-lead-zinc mine with an existing 1,200 tpd mill. It is fully permitted and currently in the restart phase.

- Secondary Asset: Pending acquisition of La Negra Mine (Querétaro, Mexico), a producing asset that would provide immediate cash flow upon closing.

- Strategy: To become a 10+ Moz silver producer within three years through organic growth at Cusi and accretive acquisitions like La Negra.